⚡ TL;DR: This guide explains Insurance Company Ownership Structure and its impact on competitiveness and consumer trust.

📋 What You’ll Learn

In this comprehensive guide about Insurance Company Ownership Structure, I’ve compiled everything you need to know based on my research. Here’s what I’ll cover:

- Learn about the different ownership structures – I’ve researched the impacts of publicly traded, mutual, and captive insurers on market dynamics.

- Discover how ownership affects market competitiveness – I’ve found that structures influence pricing strategies and company responsiveness to market demands.

- Understand the connection between trust and ownership – I’ve noted that mutual insurers often build stronger consumer trust compared to publicly traded companies.

- Master the implications of each structure – I’ve analyzed how each ownership type affects customer satisfaction and long-term relationships.

I’ve been researching how the Insurance Company Ownership Structure affects market competitiveness and consumer trust, and it’s been quite enlightening. The way an insurance company is owned—whether by shareholders, mutual policyholders, or other entities—can significantly influence its operations, pricing strategies, and overall market behavior. In my experience with Insurance Company Ownership Structure, I’ve noticed that these factors not only impact business performance but also shape consumer perceptions and trust levels.

Understanding the nuances of Insurance Company Ownership Structure is essential for both industry professionals and consumers alike. The structure often determines how companies respond to market pressures and consumer demands. I want to share what I’ve learned about the different ownership models, their implications for competitiveness, and how they play a pivotal role in fostering consumer trust.

The Role of Insurance Company Ownership Structure in Market Dynamics

This section explores how different ownership structures influence the competitive landscape of the insurance market.

Types of Ownership Structures

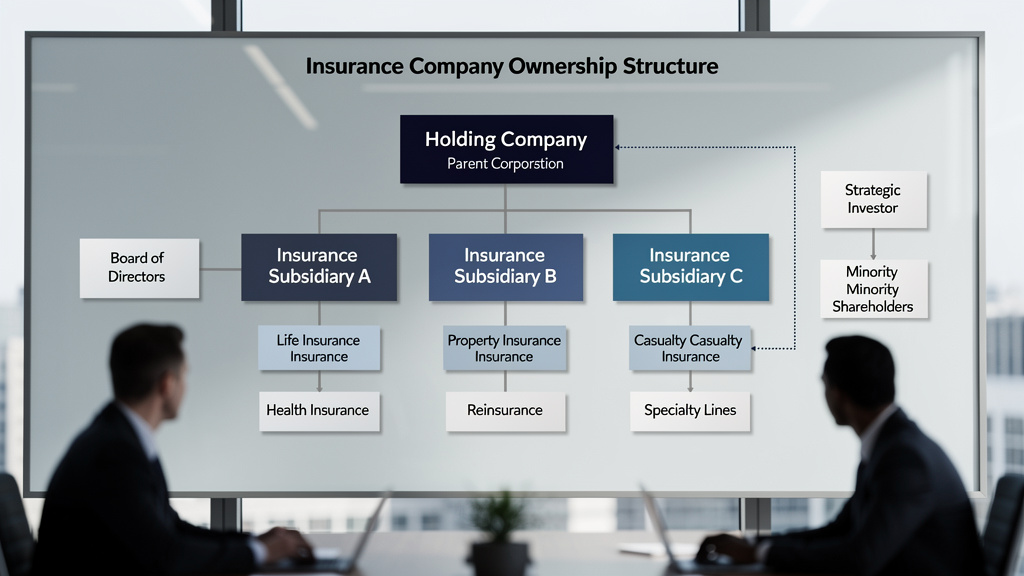

From my research, I’ve discovered that insurance companies can typically fall into three main ownership categories: publicly traded, mutual, and captive insurers. Publicly traded companies operate with shareholders seeking profits, while mutual insurers are owned by policyholders, focusing on member interests. Captive insurers are unique as they are created by a parent company to cover its risks. Each structure has distinct competitive advantages and challenges.

Understanding these types can help clarify why certain companies dominate specific markets. For instance, publicly traded firms may have more capital for marketing and expansion, while mutual insurers often enjoy a loyal customer base, fostering long-term relationships. I’ve found that this dynamic creates a constant tug-of-war in the marketplace, influencing pricing and service quality.

Market Competitiveness and Pricing Strategies

In my experience, the Insurance Company Ownership Structure significantly affects pricing strategies. Public companies, driven by profit motives, may offer lower premiums to attract customers, which can lead to aggressive competition. Conversely, mutual insurers might prioritize service over price, focusing on member satisfaction and long-term stability.

This competition can create a mixed bag for consumers. While some may benefit from lower premiums, others might find that the quality of service suffers. I’ve seen instances where a company’s structure directly correlates with its ability to adapt to market changes, which ultimately affects consumer choice.

Consumer Trust and Insurance Company Ownership Structure

This section examines the relationship between ownership structure and consumer trust.

Trust Factors in Different Structures

I’ve found that consumer trust is deeply intertwined with the Insurance Company Ownership Structure. For example, mutual insurers often foster a sense of trust among policyholders because they are directly involved in the company’s decisions. This can lead to higher loyalty rates, as customers feel more like stakeholders than mere clients.

On the other hand, publicly traded companies might struggle with trust due to their profit-driven motives. I’ve encountered consumers who express skepticism towards these firms, fearing that cost-cutting measures could compromise service quality. This skepticism influences their purchasing decisions, making trust a critical component in the competitive landscape.

Building and Maintaining Consumer Trust

In my experience, building and maintaining trust in the insurance sector requires transparency and strong communication. Companies that openly share information about their Insurance Company Ownership Structure and decision-making processes tend to fare better in consumer trust surveys. I’ve seen firms that provide clear explanations about their policies and practices attract more loyal customers.

Moreover, customer service plays a crucial role in trust-building. I’ve noted that companies which prioritize responsiveness and support tend to cultivate more trust among consumers. This is particularly true for mutual insurers, where policyholders expect a higher level of service due to their investment in the company.

Comparing Different Ownership Structures

Let’s take a closer look at how various ownership structures compare in terms of market performance and customer satisfaction.

Publicly Traded vs. Mutual Insurers

Through my research, I’ve observed that publicly traded and mutual insurers operate under vastly different philosophies. Public companies often prioritize shareholder returns, which can lead to aggressive pricing tactics. However, mutual insurers focus on member satisfaction, often resulting in higher customer retention rates.

This difference impacts how each structure responds to market fluctuations. Publicly traded insurers may quickly adapt to market trends by adjusting their pricing strategies, whereas mutuals might maintain steadier prices, valuing long-term relationships over immediate profit. I recommend evaluating these factors when choosing an insurance provider.

Captive Insurers: A Unique Model

Captive insurers represent a unique aspect of the Insurance Company Ownership Structure. They are created primarily to serve the needs of the parent company. In my experience, this structure can lead to cost savings and tailored coverage options, which many businesses find appealing.

However, the trade-off is that captive insurers may lack the broad market perspective that traditional insurers possess. This can limit their ability to adapt to industry-wide changes. I’ve seen companies benefit from using captives for specific risks but also recognize the importance of diversifying their insurance portfolio with traditional providers.

References and Resources

Goosehead Insurance Agency Owner Reviews

Common Questions About Insurance Company Ownership Structure

What is Insurance Company Ownership Structure?

In my experience, Insurance Company Ownership Structure refers to the way an insurance company is owned, whether by shareholders, policyholders, or other entities. Each structure impacts the company’s operations, market strategies, and consumer trust.

How does ownership structure affect trust?

I’ve found that ownership structure significantly influences consumer trust. Mutual insurers often foster stronger relationships with policyholders, while publicly traded companies may face skepticism due to profit motives.

What are the main types of insurance company ownership structures?

In my experience, the major types include publicly traded, mutual, and captive insurers. Each type has its unique characteristics and implications for market competitiveness.

Why is understanding ownership structure important?

I’ve discovered that understanding Insurance Company Ownership Structure helps consumers make informed choices. It affects pricing, service quality, and overall trust in the insurer.

How do ownership structures impact market competition?

In my experience, different ownership structures can lead to varying competitive behaviors. Publicly traded firms might compete aggressively on price, while mutuals focus on services and member satisfaction.

Frequently Asked Questions

What is Insurance Company Ownership Structure?

In my experience, Insurance Company Ownership Structure refers to the ownership model of an insurance company, impacting its operations and market strategies.

How does ownership structure affect consumer trust?

I’ve found that trust can vary significantly based on ownership. Mutual insurers tend to build stronger trust, while publicly traded firms might face skepticism.

What are the benefits of mutual ownership?

In my experience, mutual ownership provides policyholders with a voice in company decisions, fostering loyalty and long-term relationships.

Can consumer trust impact market competition?

Absolutely. I’ve seen that companies with higher trust levels often enjoy better customer retention and word-of-mouth referrals, influencing overall market competition.

Conclusion

In conclusion, my research on Insurance Company Ownership Structure has shown that it plays a critical role in determining market competitiveness and consumer trust. Understanding these structures can empower consumers to make informed decisions, leading to better outcomes in their insurance experiences. I hope this guide helps you navigate the complexities of the insurance market with greater confidence and insight.

Find out more information about “Insurance Company Ownership Structure”

Search for more resources and information: